China travel industry is growing very fast in recent three years. With the popularity of the internet and digital technology in China, travelers have more and more channels to gather all travel related information, which are being provided by different service players to meet very personalized needs from customers. Especially, the combination of internet and travel industry is generating new opportunities beyond the traditional business model. Airlines, as one of the key traditional service providers, are facing huge challenges to firstly meet the needs of demanding customers and secondly re-position themselves in this new travel eco-system.

To gain a better position in this eco-system, airlines have to embracing the digital transformation to refine their business model as well as the way they deal with customers and partners. It is important to develop a new digital strategy and integrate internal operations to be aligned with the transformation. Airlines have to realize that the internet is changing people’s behavior quickly and drastically and the only way to deal with this is to change and transform themselves to new digitalized players in the market.

Airlines’ Profit Challenge

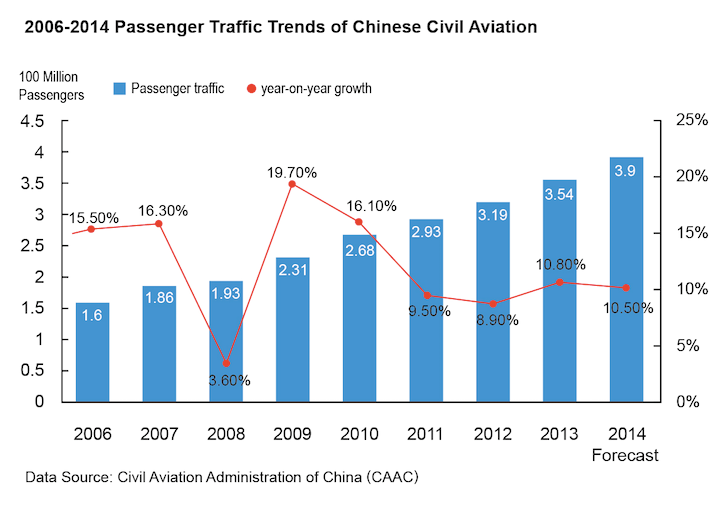

In 2013, the International Air Transport Association (IATA) announced global air passenger transport volume had reached 3.1 billion passengers; around the same time, the Civil Aviation Administration of China (CAAC) announced that its national aviation passenger volume had grown to 351 million passengers. Yet even with these massive numbers, the volume growth in China’s aviation passenger transportation market slowed significantly to only about 11.5% (compared with 20% in 2009 and 16% in 2010). The European debt crisis, domestic economic structural adjustments, and other factors all have affected demand growth. In turn, the three largest airlines also suffered weak transport volume growth and shrinking profits. Between January and September 2013, the net profits for Air China, China Eastern, and China Southern were 3.3%, 2.7% and 1.9%, respectively, whereas the net profits for American Airlines and Delta were 5% and 7%. These weaker profits for China’s domestic airlines, compared with U.S. airlines, largely reflect depreciation in RMB interest and high labor and fuel costs, as well as furious competition in China’s market, which has squeezed airlines that traditionally competed through pricing optimization, despite the limited power for profit improvements through price-based competition.

From a net profit rate perspective, even for global, large, market-leading airlines, profits are limited. China's airlines also are affected by human costs, economic stagnation, and competition from global airlines and the open sky policy. If government subsidies someday become "stingy," can China's airlines overcome their low profit rate and weak growth? We address this question by investigating the basic attributes of the product offered to airline passengers: the delivery of intangible products and services through a complex, long process, with profits affected by multiple factors: the price of oil, airport locations, aircraft costs, labor costs, and severe competition.

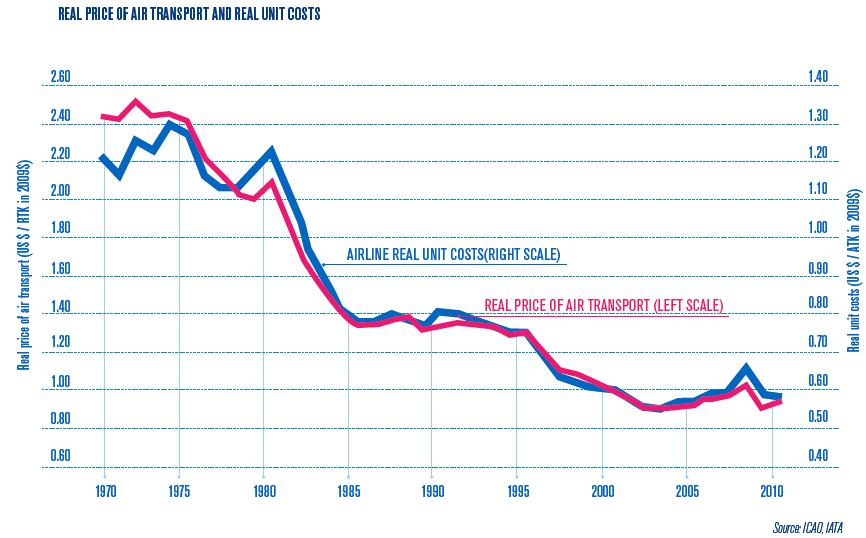

To improve profits, airlines might reduce their operational costs, but doing so cannot provide new revenue opportunities, nor does it change the business model, because costs cannot be reduced endlessly. Airlines must develop ways to generate new revenue at a higher profit. Between five and eight years ago, U.S. mainstream airlines began to adjust their traditional service and product offers, insert more value added to ease margins and gain profit, and avoid pressures imposed by widely used low cost carriers. These experiences revealed three key insights: (1) Without ancillary services/products, airlines’ net profit would be negative, so ancillary revenue is important to airlines; (2) the net ancillary profit normally is much higher than that associated with a ticket and therefore greatly contributes to improving the bottom line; and (3) ancillary items help airlines provide personalized services to customers, beyond ticketed services.

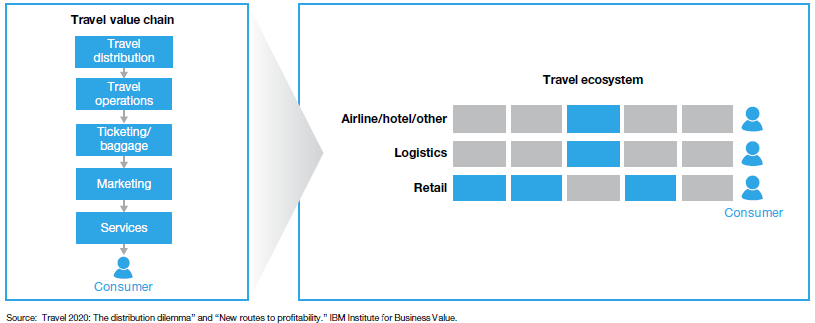

The profit structure of the travel ecosystem shows that airlines suffer the worst profits, whereas travel agencies (including online versions) earn the greatest net profit. The reason is simple: Customers value intelligent travel advice and end-to-end user experiences, not the carrier that merely transports them from location A to location B. Therefore, they tend to spend more on travel services, other than a ticket or a hotel room, which leads to the notable net profit difference between upstream and downstream members of the travel industry value chain. If airlines want to develop more revenue opportunities and improve their profits, they need to explore and expand their business service areas across the industry, to increase their portion of the wallets of travelers.

The Travel Ecosystem

Traditional travel ecosystems and value chains were stable, offering limited customer choices. With the emergence of the Internet, service providers discovered a new and exciting way to approach and interact with customers directly, though they mainly exhibited a sales channel perspective. As customers grew more empowered by digital equipment though, their behaviors also changed drastically. The Internet is more than simply a sales channel, especially in the guise of the mobile and social media networks that now dominate the ways people communicate with one another. Without the development of digital technology, the industry ecosystem would not have changed to look the way it does today. This change has arisen in a very short timeframe and seems likely to continue moving forward. Therefore, any effective analysis must look ahead, not just at the current status, to prepare for continuous digital transformations in the integration of business and technology.

We first consider and define a travel ecosystem. A travel ecosystem consists of the players that make up the travel value chain and that depend on one another. In the past, due to non-transparent information and technology barriers, travel service providers—airlines, hotels, travel agencies—controlled the majority of the value chain and held significant bargaining power. The ecosystem consisted of clear upstream and downstream sectors. Thus, it was difficult to provide or receive personalized services, especially from the customer perspective. However, the rapid development of the Internet and mobile and social networks gradually broke down information barriers, providing easy access to and by customers. Whereas in the past, value chain profits were shared by airlines, Global Distribution System (GDS), and offline tour operators, today the Internet and online travel providers have dramatically changed the situation. In this complex network, especially in China, the value chain has flourished to encompass travel desire, planning, product search, reservations, destination services, en-route services, and post-travel reviews—that is, to become a complete travel ecosystem, in which both the service and its value are micro-segmented in a very detailed way.

In this travel ecosystem, online travel markets are rich and complex, as exemplified by BATX’s market layout. In 2013 and 2014, BATX used capital instruments to build its own travel platform and acquire different components, including Baidu’s search capabilities, Ali's selling features, and Tencent's social media as entry points. Then it devised its own unique travel ecosystem to generate more value for customers while also increasing the partner companies’ profits. This type of cross-industry synergy strategy tends to be very successful.

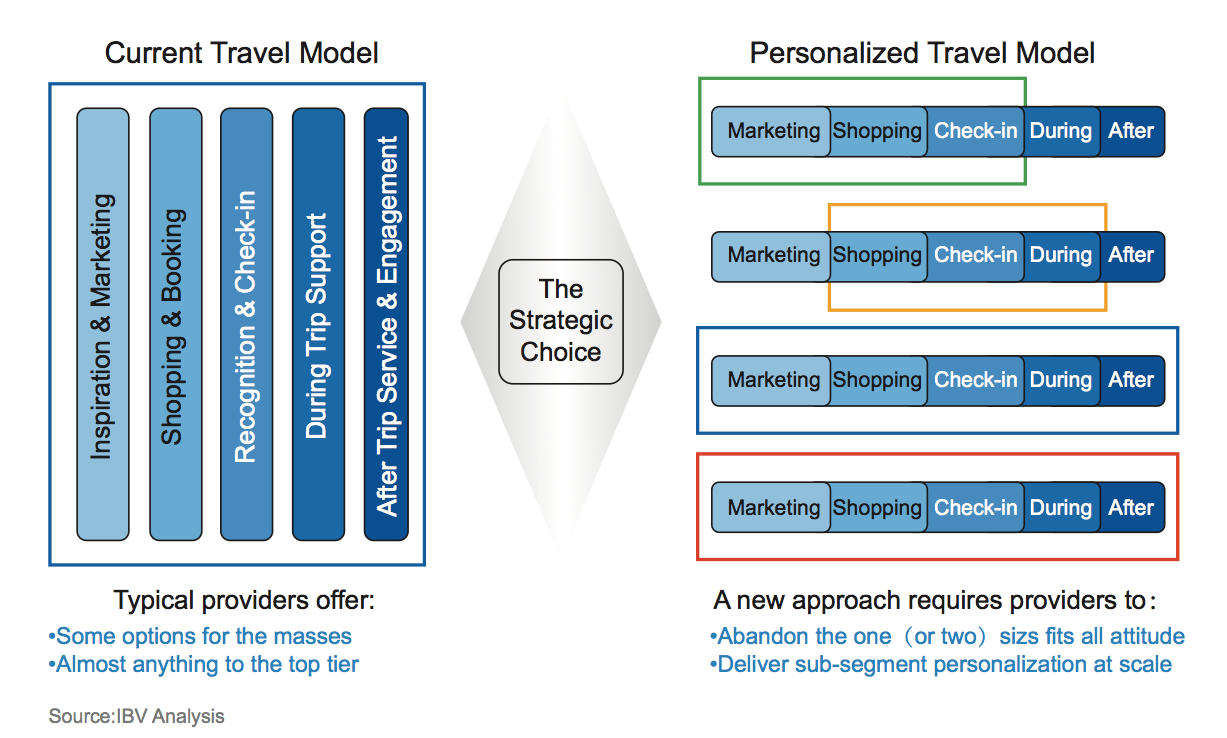

Modern travelers have vastly more choices than ever before, throughout their journey, because so many reachable, niche service players provide specific offers to meet the needs of the different segments of customers. The “one process fits all” strategy no longer works; it has been replaced by a “you pick what you need” model that enables travelers to satisfy their individual needs during the trip. Obviously, airlines cannot provide all the services themselves, but digital technology makes it possible for them to partner with various travel service providers and serve customers with a package or even an a la carte model that could increase the airlines’ revenues and profits.

In this environment, airlines essentially have been backed into a corner, dismissed as “just carriers” that offer commodity products and must compete on price, which means they also contribute to online travel providers’ high profits. Airlines’ bargaining power has declined, and their profits continue to be squeezed to the extremes. Relying on traditional route resources and single product service models cannot improve the lot of airlines, though they also struggle to build competitive advantages in the current Internet-dominated environment. Is the future unavoidably bleak then?

Changes by Leading Global Airlines

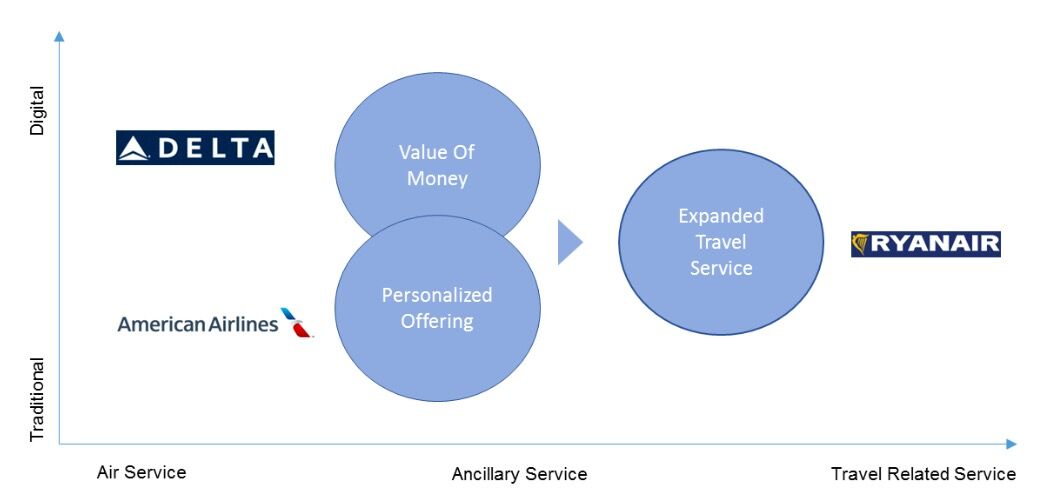

Consider the “inventor” of the computer reservation system, American Airlines (AA). It had previously innovated airline-related information technology, by developing the first host-based ticket reservation system, which eventually evolved to become SABRE (a global distribution system company). In this new digital world, AA seeks to use the Internet to transform its distribution model by building direct connection products with travel agencies. With this set-up, AA can sell more ancillary services with more flexible sales of AA-exclusive products, tourism packages, and additional services, which in turn increases its revenues and mitigates the negative effects of downturns in its traditional ticket margins. Therefore, AA improves its bottom line and can offer more customized services to customers, including those available through its own digital channels.

Delta Airlines aims to enhance customer value by using new digital technology to enhance the travel experience across all of Delta’s touch points. Spanning these points, Delta offers customized products and value-added services to customers, which generate more revenue for Delta while also improving customers’ travel experiences. This critical strategy is helping Delta improve its profits, because it sells high margin ancillary services that ultimately contribute to its financial bottom line.

Ireland’s Ryanair is attempting to prove that airlines can rebuild to instill Internet/digital technologies into their business models. Branded as a low cost airline, Ryanair aggressively provides different travel services to customers by leveraging its vast passenger volume and the low price of its standard product (i.e., ticket). In 2013, its ancillary sales revenue accounted for 22% of its total revenue—a terrible ratio for an airline with its scale. Thus in early 2014, Ryanair and Google reached a strategic agreement to build GOOGLE FLIGHT SEARCH, which aims to bundle Ryanair products with Google’s search volume.

As these examples show, airlines are adopting different strategies to embrace digital trends and address the challenges of the new travel ecosystem. Despite the pressures imposed by business operations and the burden of their existing assets, their advantages also are obvious: They have frequent and real physical connections with customers, because travel services inherently must be delivered through an interactive experience during a lengthy journey. As the practices and innovations of AA, Delta, and Ryanair show, airlines branded as “traditional carriers” are leveraging their core advantages, giving them more opportunities to interact with customers across the journey and generate more effective services and revenue opportunities. We note two main insights:

The Internet and digitalization must be integrated into airlines’ operations and business models, rather than remaining a nice-to-have possibility. For AA, Delta, and Ryanair, anywhere from 40%–75% of their sales come through the Internet. Whether airlines want to accept it or not, Internet capabilities will define competition and remodel both airline strategies and their markets.

Whether it means opening their channels to improve revenue opportunities (e.g., AA), creating more valuable services to increase profits (e.g., Delta), or providing more integrated travel services for high-volume, “low-price” passengers (e.g., Ryanair), airlines must refine their corporate strategies to instill a digital “gene” into their bodies.

Embracing the Digital Transformation and Innovation

Can airlines lead travel ecosystems and share a bigger piece of the pie? The answer depends less on what they lack but more on how well airlines leverage their traditional advantages and integrate them with new digital trends. We propose four “integrations” airlines could adopt to support their digital transformation.

Integrate the digital strategy with the corporate strategy

Airlines must revisit their corporate strategy to evaluate how new trends are affecting their overall company strategy and business models. Airline customers are equipped with vast digital “weapons” and are much better informed than ever before. Thus airlines need to refine their strategies, not just add on some technology components to their operations; the digital change is not just an evolution of technology but an actual shift in customers’ behaviors. Furthermore, airlines need to develop their new business models in digital contexts, with open minds, because increasing passenger volume is just the first step. Throughout the entire travel journey, airlines should identify and leverage their great opportunities to generate travel-related revenue streams.

Integrate technology and business into one organization

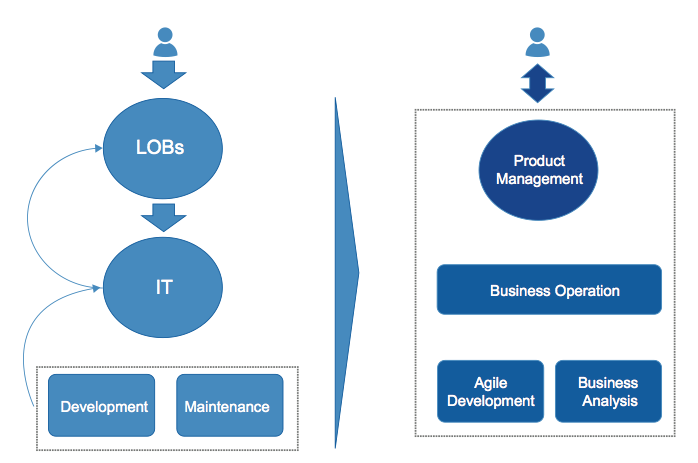

In the past, information technology and business lines were separated, with technology operating behind the scenes and often lagging behind business requirements. Responses to the market rarely occurred in “real time” but rather required a sometimes lengthy lead time. Such lead times are no longer possible with customers who understand the technology, especially the intelligent equipment and online services provided by pure Internet players. Airlines need to become more agile and technically driven. From this perspective, previously separated technology and business lines need to be integrated quickly to meet or even drive customers’ needs, without any lengthy delays. Because business is being managed digitally, technology and business cannot be separated. If they are, airlines cannot meet the quickly changing demands of customers.

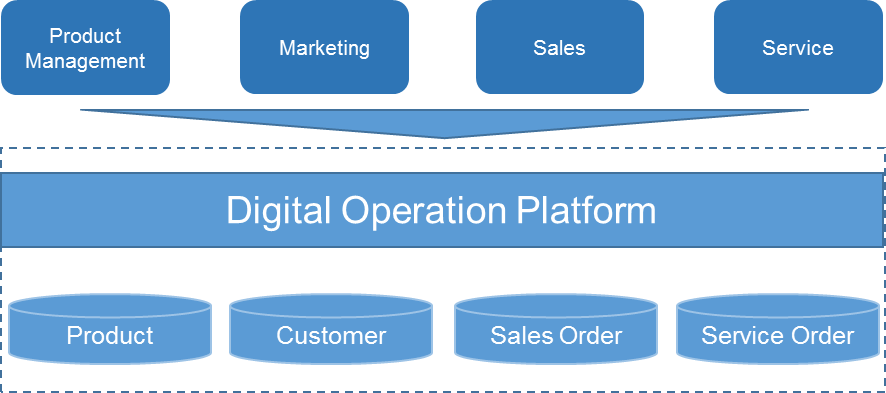

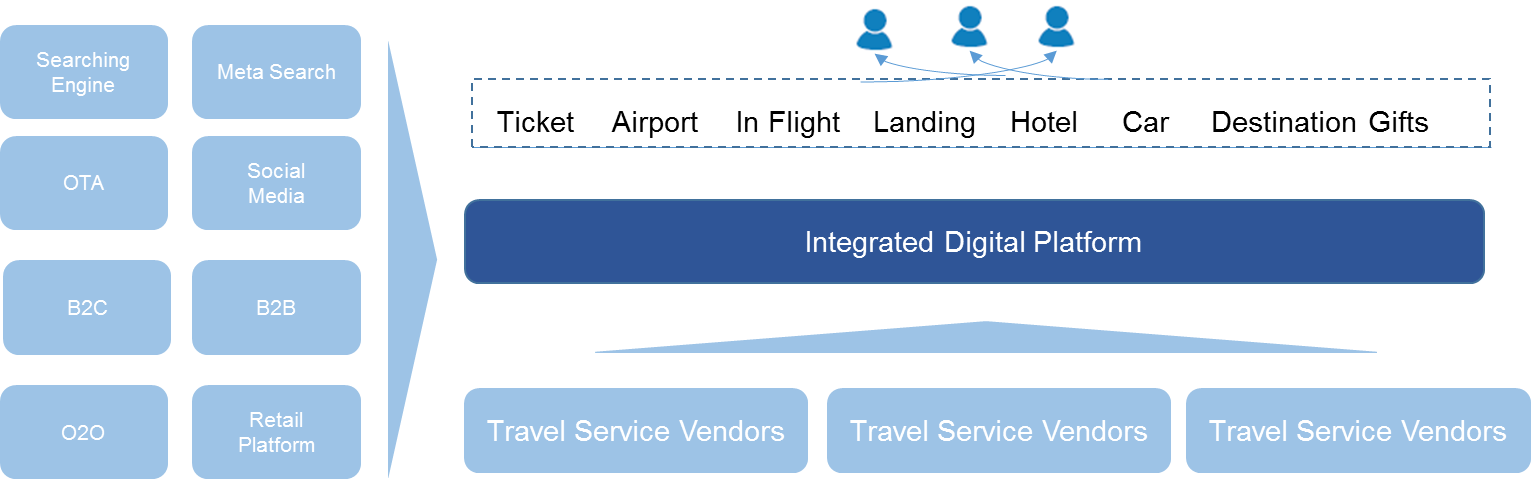

Integrate product, marketing, sales, and service on one digital platform

The four main functions of airlines—product management, marketing, sales, and service—traditionally operated in four silos, without transparent information sharing among them, partly because their integration would have been costly and complicated. Thus, the customer experience and strategy were not aligned. In a digital world, the Internet and mobile technology make information integration easier. Accordingly, airlines need to build integrated platforms that provide customer information, product offerings, marketing campaigns, sales promotions, and transactions, as well as centralize all service delivery information to be shared across the four functions. An integrated platform and centralized data repository in turn support the airline’s integrated organization and ability to respond quickly to the market and customer needs.

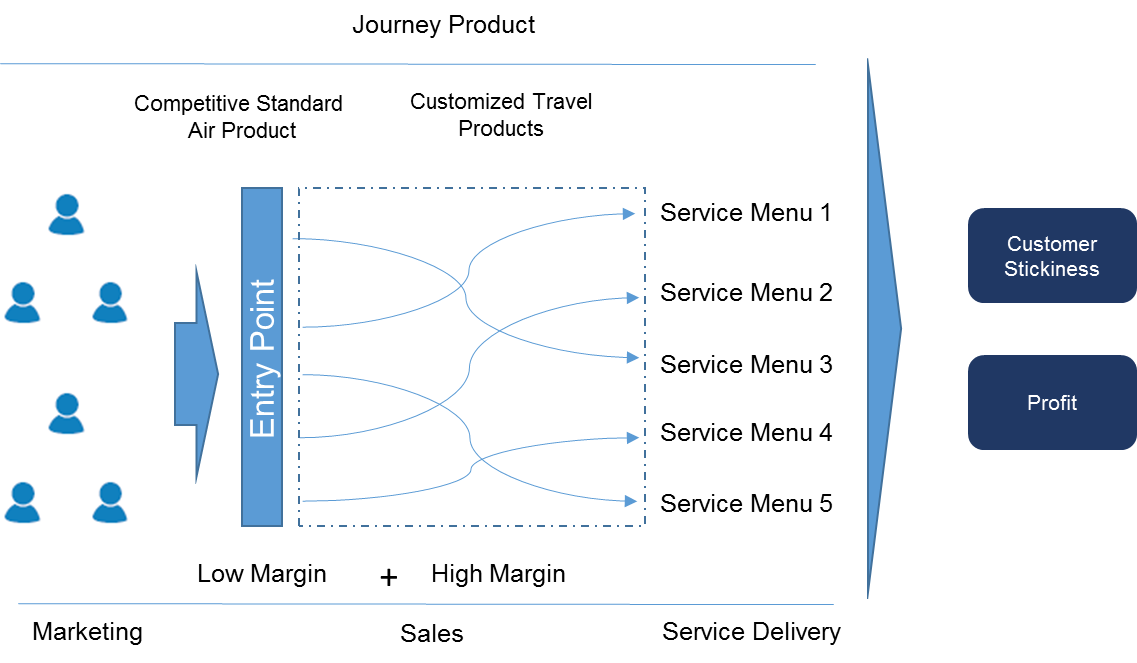

Integrate air and non-air service into a single travel service management

The traditional method for designing airline products focused only on the airline ticket, rather than the whole travel journey from the customer’s perspective. Today, with digital technology, airlines can easily integrate and partner with various travel resources, such as cars, hotels, destination tours, and other travel-related services. Therefore, when modern airlines design their product offers, they can achieve an end-to-end service product, which in turn enables them to promote different product packages to unique customers, with the assistance of a digital platform with strong integration capabilities.

Unfortunately, airlines face a rapidly changing world, an uncertain business environment, and increasingly demanding customers. Yet we believe they have many reasons to be optimistic, because airlines have inherent advantages, due to their interactions with customers during service delivery and their chances to integrate more travel resources, beyond transporting passengers from location A to location B. For these competitors, the question is clear: Do they want to stick to a simple carrier business, earning low margins, or would they prefer to be travel innovators, bringing more value to travelers and thus earning more profit for the company?

(The author is Allen Cai, Air and Travel Sector Leader, GBS GCG at IBM.)